The first time Amelia Howells ever wrote a check, she was 28 years old and standing in a Connecticut apartment leasing office, with no idea what to do.

The British expat had just moved to the U.S.; she’d never had to write a check in London or during her seven years in Switzerland.

“I had to sit down with a woman to learn how to do it. She thought it was hilarious and called in all the other people in the office to have a laugh at me,” she recalls. “In Switzerland, they don’t even have checks. We did all our rent and utilities online, and that was back in the early 2000s.”

In an era of smartphones, online banking, and Venmo transfers, the U.S. still can’t seem to wean itself off paper checks. In most countries, they’ve gone the way of the fax machine and the rotary telephone. But their demise isn’t coming to America any time soon.

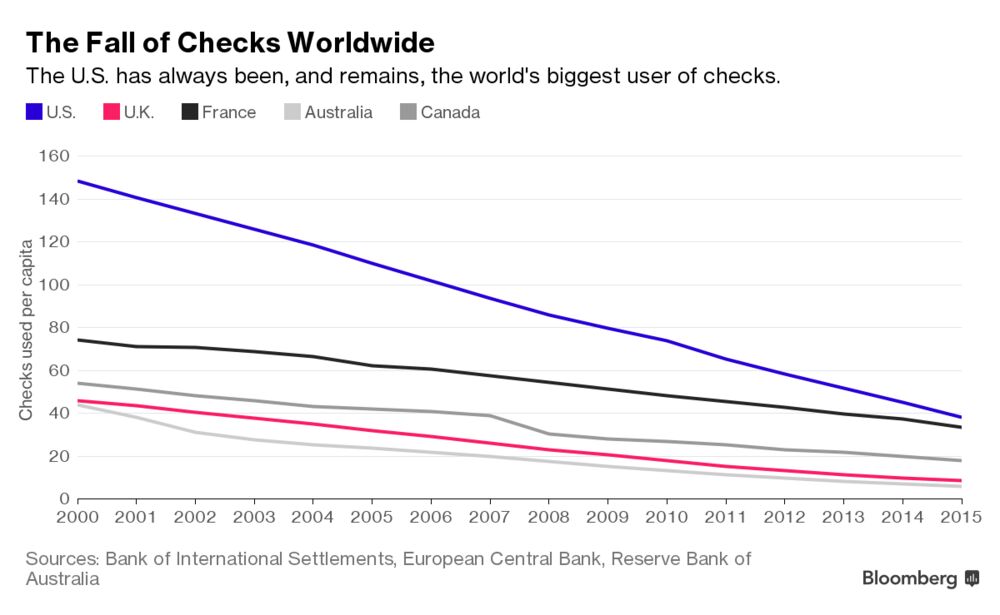

Americans still reach for their checkbooks more than anybody else. In 2015, they each made 38 check transactions, on average, according to data from the Bank of International Settlements, the coordinating body for the world’s central banks. Compare that with about 18 in Canada, just 8 in the U.K., and almost zero in Germany. The only country with anywhere close to American numbers is France.

There are, of course, cheaper, faster, and more efficient alternatives. Electronic transactions clear quickly—no stamp or envelope needed—and cost their users about a 10th as much as checks to process. (A 2015 survey of businesses by the Association for Financial Professionals pegged the median cost of issuing a check at $3, compared with under 30 cents for a electronic transaction.) That’s not even taking into consideration that box of replacement personal checks, which can cost a consumer more than $20. Using peer-to-peer payment apps to transfer money between checking accounts, however, doesn’t incur fees.